![]()

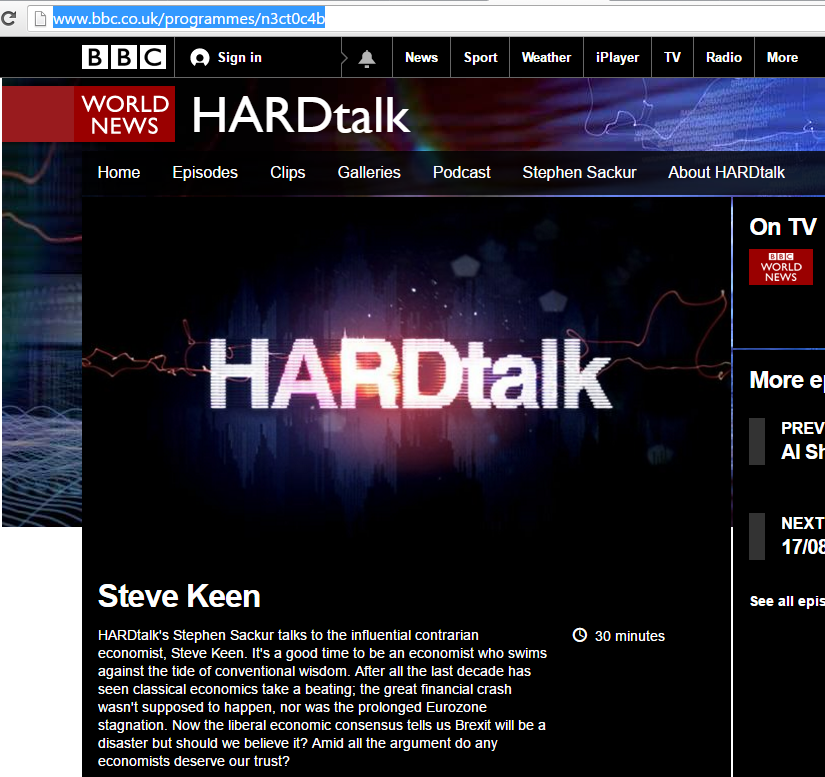

This interview, which was just recorded today, will go to air tomorrow. The broadcast details are:

BBC News Channel: 02.30 BST, 04.30 BST and 20.30 BST Tuesday 16th August 2016, and 00.30 BST Wednesday 17th August 2016

And from the 04.30 TX it will then be available within the UK on BBC iPlayer for one year.

BBC World News Channel: 03.30 GMT; 08.30 GMT; 14.30 GMT and 19.30 GMT Tuesday 16th August 2016

It will also go out at numerous timeslots on Friday on the BBC World Service.