![]()

This blog entry first appeared as a feature in the Daily Telegraph on Wednesday April 9th 2008. If you’re a newcomer to it courtesy of that feature, and you want to look at this issue in more depth, there are links below to more detailed analysis.

The Daily Telegraph lived up to its nickname of “The Daily Terror” last week, with a frontpage attack on Reserve Bank of Australia Governor Glenn Stevens entitled “Is he Australia’s most useless?”, and an editorial that was no less provocative: “RBA boss is losing interest”.

It would be easy to criticise the Telegraph’s comments on the technicalities, many of which they got wrong (I’ll outline some of those below). But what I saw behind the comments was a sense of frustration that, I believe, is justified.

Why? Because over a decade ago, our Government ceded control of monetary policy to the RBA, in keeping with a worldwide belief that “Central Bank Independence” would result in better monetary policy. We were told that if we took monetary policy out of the hands of the politicians, and handed it over to the experts, the financial system would work a lot better.

If that’s the case, then something has gone terribly wrong. Far from giving us stability, the period of Central Bank Independence has ushered in an unprecedented financial crisis, and extreme financial hardship for many ordinary working families (to use a Kevinism).

This is what motivated the Telegraph’s ire—especially since Stevens’s testimony appeared to downplay both the seriousness of the crisis, and the damage that a dysfunctional financial system has done, and is doing, to the rest of society.

Stevens’s testimony emphasised the RBA’s role in fighting inflation above all else. But the broad job description of Central Banks is to ensure the soundness of the financial system, and on that Central Banks worldwide have clearly failed.

Think about it. If this policy had been successful, then the Daily Telegraph’s spray wouldn’t have happened, because finance would have been on the boring back pages of the paper.

So how did Central Banks get it so wrong?

Largely because they followed accepted economic theory about what their role should be. At the time Central Banks were allowed to set monetary policy independently of governments, the conventional economic wisdom was that they should:

- ignore stock and housing markets;

- forget about trying to control the money supply;

- deregulate the financial system to make it more efficient; and

- just use short term interest rates to control inflation.

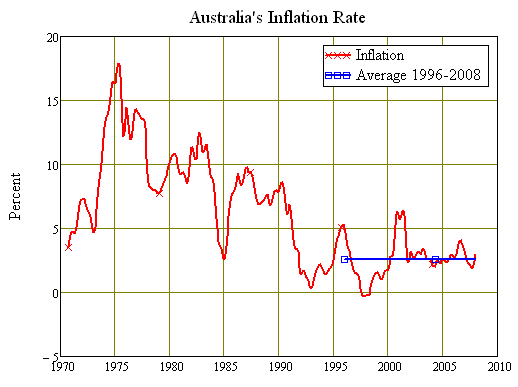

If their success is measured solely on the front of controlling inflation, then the RBA has met its target of keeping inflation in the range of 2–3 percent over the medium term. The average value from 1996 till now is smack in the middle of this range.

However, while the part of the system that Central Banks have focused on has done pretty well, the rest has gone to hell in a handbasket.

The finance markets were overtaken by alchemists who promised to turn lead into gold—or subprime mortgages into AAA secure bonds. Instead, they delivered lead aplenty to borrowers and investors, and absconded with the gold themselves. Debt reached levels that have never occurred before in human history. Asset prices reached unsustainable (and for housing, unaffordable) levels, and are now crashing, and taking peoples’ housing and livelihoods with them.

It’s worth getting a handle on just how badly the period of Central Bank Independence has gone wrong—and not only in Australia.

The Great Depression began with private debt levels in the USA equal to one and a half times its GDP, and then deflation—falling prices—and falling output drove it up to 215 percent by 1932. Today, US debt is 280 percent of GDP.

Australia peaked at 77 percent of GDP in 1932; we’re already at 165 percent—when the RBA appears to think everything is functioning well. And another 14 major OECD countries are in the same pickle (the only major exception is France).

Asset prices are also simply crazy.

The best measure here is to compare them with the consumer price index, and on that basis US house prices bubbled from 12 percent above the long term trend, to 120 percent above it in the first ten years of Greenspan’s independence.

Our housing price bubble was even worse than that, and though it has not yet started to deflate as has America’s—where prices have fallen 16% in real terms in the last two year—ultimately it must.

If politicians had been responsible for a policy mess like this, the press would have had their guts for garters—and rightly so. But since the so-called experts are in control, they can’t be held to account—and hence the Telegraph’s frustration, which boiled over last week.

In fact, economists aren’t experts about the economy in the same fashion that physicists are about nuclear energy. As George Soros argued recently in the Financial Times, the approach Central Banks have been following has clearly failed, and it’s time we gave a new approach a try—one that doesn’t subscribe to the myth that the best market is a deregulated one.

The errors in the Daily Telegraph’s article

The RBA’s job isn’t to tell banks what to charge on mortgages. The one rate they have control over is the inter-bank rate, which is used when one bank has to pay interest to another when their accounts don’t balance. That sets the floor for short term rates–and the RBA supplies as much liquidity as it needs to make sure this rate applies.

Then banks set their own longer term rate in accordance with this base rate and market conditions. In the recent past, competitive pressure from non-bank lenders made the gap between the (short) RBA interest rate and (long) mortgage rates the lowest they’d ever been–but much of that reflects what is now euphemistically called “a mis-pricing of risk”.

The dilemma for the bank is that the credit crunch has caused this once narrow gap between short term and long term rates to balloon–and there’s literally nothing they can do about it. In one sense, it helps keep banks solvent–since they make money from the spread between short and long term interest rates–but it makes the RBA even less able to influence mortgage rates.

The Commonwealth Bank also didn’t increase its rates just because of Stevens’s speech. They would have done their calculations about their increased cost of funding courtesy of the credit crunch, and how much this was costing them, well before the speech. Maybe it did however make them think that “now’s the time” to move on it.

The real issue, as I outline above, is that the era of Central Bank Independence hasn’t “taken finance off the front pages”, but made it front and centre with the biggest financial crisis in world history.

Further reading

- This blog. I started it one and a half years ago, when I concluded that a serious debt-driven financial crisis was inevitable, and someone had to raise the alarm about the possibility of one happening. Here you will find:

- The Debtwatch Report (21 to date) which come out just before the RBA meets each month to set rates, and takes a topical look at economics and the rate decision in particular;

- Academic papers that focus on the topics of debt deflation and the monetary system;

- A Podcast recorded after each DebtWatch report by Stuart Cameron of Rife Media

- My report And Deeper in Debt published by the Centre for Policy Development last September.

- Debunking Economics, a website that supports my book of the same name, and stores my lectures on economics and finance at the University of Western Sydney.

- The most relevant lectures to explain the approach I take to finance are those on Financial Economics

- The most accessible lectures on my non-orthodox approach to economics in general are those on Managerial Economics

- Blogs by other commentators whom I believe have a handle on what has happened. For a decade or more, these writers have been “contrarians”, railing against the stupidity of Wall Street and accommodative Central Banks while the rest of the pundits applauded such financial innovations as … subprime loans:

- Doug Noland and the Credit Bubble Bulletin for the Prudent Bear mutual fund;

- iTulip, a website first set up by Eric Janszen to critique and satirise the Internet Bubble, and revived when the US housing bubble supplanted it. Eric frequently interviews academic and industry specialists; check out in particular:

- Interview with Michael Hudson and his analysis of what he terms the “FIRE Economy”–Finance, Insurance and Real Estate

- My interview on the Financial Instability Hypothesis

- Robert Shiller’s excellent empirical analysis. Robert coined the phrase “irrational exuberance” that was later made famous by a speech by Alan Greenspan–who unfortunately understood the issues there about as well as Donald Rumsfeld understood Iraq.

- Shiller maintains a historical database on finance, with freely downloadable data

- The US Housing Crash Blog

- Global House Price Crash Blog

- Housing Affordability Blog

- Lest it be thought that I’m a critic of everything the RBA does:

- Most of my Australian data comes straight from the RBA Bulletin Statistical Tables

- The RBA Conference on Asset Prices and Monetary Stability has some excellent papers. I only wish that the orientation set in this conference had guided subsequent RBA policy.

- This RBA paper comparing the Great Depression to the 1890s Depression is one of the most informative historical analyses I’ve ever read

- Ditto for the US Federal Reserve. While I believe that the “Greenspan Put” has encouraged “moral hazard” behaviour that has made this the worst financial bubble ever, the Fed has also been a bastion of free and accessible data. My US data largely comes from its Flow of Funds report.